Pregnancy Insurance: Guide to Health Coverage for Expecting Parents

All major medical insurance plans today cover pregnancy. This coverage includes prenatal care, inpatient services, postnatal care, and newborn care. These essential services were put in place by the Affordable Care Act and help make it easier for both planning and expectant mothers to get insurance.

However, it’s still important to understand how health insurance works concerning pregnancy, since every pregnancy is different and will incur different costs. If you don’t have insurance and are pregnant, you may qualify for government health insurance programs, and if you don’t, there may be free or discounted care options available to you in your area. Continue reading to learn more about getting health insurance while pregnant and how much insurance covers when having a baby.

Importance of health insurance during pregnancy and childbirth

Health insurance during pregnancy and childbirth is essential because it covers the costs of prenatal check-ups, delivery, and postnatal care, ensuring that expectant mothers receive comprehensive medical attention without the financial burden. Prenatal care helps monitor the health of both mother and baby, while insurance also addresses the substantial expenses related to labor and delivery. Additionally, postnatal care and follow-up visits are crucial for a healthy start to motherhood. Without insurance, these costs can be overwhelming, potentially discouraging individuals from seeking essential care, making health insurance a vital safety net for expectant families.

The costs of maternity

Prenatal care and giving birth is expensive. According to Peterson-KFF Health System Tracker, the average cost for a vaginal delivery was $14,768 ($2,655 of which is typically paid out-of-pocket) and a cesarean section was $26,280 ($3,214 of which is typically paid out-of-pocket) from 2018-2020. The cost of giving birth varies greatly. For instance, it is estimated that pregnant women from the ages of 15-49 enrolled in large group health plans typically incur an average of $18,865 more in health costs than women who don’t give birth. The additional spending is associated with the costs accrued from $16,011 typically paid by insurance and the remaining average out-of-pocket cost of $2,854.

Insurance typically covers a good portion of these expenses, but families may still need to be prepared to cover thousands in remaining costs. How much you pay out-of-pocket for coverage will vary depending on if you’ve met your deductible, if you have copays or co-insurances, if you’ve gone out-of-network, and other factors.

These are prices for births that go well. These averages do not include those who had complicated births or C-sections or if you or your baby requires an ICU or NICU stay. If you have complications during a C-section, you could be looking at health insurance bills totaling to around $80,000. Keep in mind that these prices do not include the cost of well-mother visits and tests, postnatal care, or newborn care.

Understanding pregnancy insurance coverage

When it comes to maternity health coverage, there are various avenues to explore, each offering different options and benefits. Understanding pregnancy insurance coverage is essential for expectant parents to ensure they have the right plan in place to support them throughout their journey to parenthood. Whether through employer-sponsored plans, government programs, or individual health insurance policies, this guide will shed light on the diverse ways you can secure essential maternity healthcare coverage.

Maternity coverage in health insurance plans

All major medical/ACA health insurance plans cover pregnancy and childbirth. Under the Affordable Care Act, pregnancy and maternity care are one of the ten essential health benefits that must be covered by health insurance plans offered to individuals, families, and small groups. Health insurance for pregnancy, labor, delivery, and newborn care became mandatory in 2014 under the ACA.

Standalone maternity insurance

Even if you don’t have health insurance, there may be free or discounted services for expecting mothers in your area. There are also affordable options such as hospital indemnity policies; however, these may not cover as many pregnancy benefits like a major medical health insurance plan would.

What does regular health insurance cover for pregnancy and childbirth?

Maternity services covered by health plans include:

- Outpatient services – These services include prenatal and postnatal doctor visits, gestational diabetes screenings, lab studies, medications, etc.

- Inpatient services – such as hospitalization, physician fees, etc.

- Newborn baby care

- Lactation counseling and devices

It’s important to keep in mind that your coverage may vary depending on what plan you have since insurers can choose how they cover these benefits. Additionally, out-of-pocket costs are dependent on several factors, such as the metallic tier of coverage you have, deductibles, copayments, and which providers you choose.

Health plans are required to provide a Summary of Benefits and Coverage documents. The summary will detail how each specific plan covers the cost of pregnancy and childbirth. If you are pregnant or plan on getting pregnant, review this summary to see how your plan – or to compare how different plans – cover childbirth, this way you will know what to expect and are less likely to get any surprise medical bills.

Keep in mind that these services are covered by major medical plans even if you got pregnant before your coverage starts. Thanks to the ACA, pre-existing conditions are covered, which includes pregnancy. It’s also important to consider that if you have a grandfathered individual health plan – this is not the kind of plan you get through your employer, it’s a plan you buy yourself – you aren’t required to cover pregnancy and childbirth. If you have a grandfathered individual health insurance plan, you may want to call your insurance company to learn about your plan’s pregnancy and childbirth coverage.

Benefits to consider when looking for pregnancy insurance

If you are pregnant or plan to become pregnant, some important things to consider about your current or any potential health insurance plan are:

- If you need a referral to see a specialist/OBGYN from your primary care physician

- The covered cost of labor and delivery

- Your copay, coinsurance, and deductible amounts

- If prenatal testing is covered – ultrasounds, amniocentesis, and genetic testing

- If you need to be preauthorized to receive prenatal care

- If non-traditional deliveries are covered – midwives and home-births (some health insurance plans consider home deliveries ‘not medically appropriate’ and will not cover them, so make sure to check with your insurer if you plan on having a non-traditional birth).

- If private rooms are covered or if you will need to share a room during hospital delivery.

Lower-cost options for pregnancy insurance

Affordable and accessible healthcare is essential for expectant mothers, and this holds true for pregnancy insurance coverage as well. If you’re currently uninsured and pregnant, it’s crucial to explore lower-cost options to ensure you receive the necessary medical care during this transformative journey. Fortunately, there are several avenues to explore, from government assistance programs to marketplace plans and Medicaid, that can provide you with affordable or low-cost health insurance options tailored to your specific needs during pregnancy. In this guide, we’ll delve into these options, helping you navigate the path towards securing essential maternity healthcare coverage without breaking the bank.

Medicaid and CHIP

If you haven’t experienced a qualifying life event but you’re looking to get affordable maternity coverage, you may qualify for Medicaid or the Children’s Health Insurance Program (CHIP). Pregnancy care and childbirth are both covered under Medicaid and CHIP. Unlike individual or family health insurance, there is no national open enrollment period for Medicaid or CHIP – which means you can enroll year-round if you qualify.

To qualify for Medicaid, you may have to meet an income requirement. Typically, those who have an annual income of 133% or below of the Federal Poverty Line (FPL) will qualify for Medicaid as they are considered “categorically needy.”

However, due to expansions to Medicaid, women who are pregnant are more likely to qualify for coverage. This means that even if you were previously denied Medicaid based on income, you might qualify now that you are pregnant as you may be considered “medically needy.”

Additionally, due to expansions to Medicaid, eligibility varies by state. If you find yourself pregnant and without health insurance, apply for Medicare pregnancy coverage, even if you think you will not qualify. However, if you don’t qualify for Medicaid or CHIP, there are still other ways for you to save money during your pregnancy and delivery.

Hill-Burton facilities and other charitable organizations

You may be able to find discounted or free care through Hill-Burton facilities or other charitable organizations, such as:

- Planned Parenthood: If you don’t have insurance, your local Planned Parenthood center may be a valuable resource for maternal care and family planning. At some locations, not all, you can receive low-cost or free prenatal care. Other family planning clinics also may be able to provide you with help during your pregnancy.

- Public Health Departments: Your local public health department may provide maternity care. They do not provide insurance, but they may be able to provide you with care relating to your pregnancy if you meet an income requirement.

- Community health centers: Community health centers provide care to those with limited access to health care. They do not provide insurance options; however they can provide you with comprehensive prenatal care. The fees for their services tend to be based on income level.

- Charity care organizations: Some organizations provide services to help women with their pregnancy. Catholic Charities and Lutheran Services are two examples of these organizations. The services offered at these charities may vary depending on location. However, services tend to range from free maternity care and postpartum care to lodging.

- Hill-Burton Facilities: According to the Health Resources and Services Administration (HRSA), there are currently 132 (as of 8/2/2019) facilities that are obligated to provide free or low-cost healthcare since they’ve accepted grants or loans provided by the Hill-Burton act. If you have a Hill-Burton Facility in your area, this may be a great resource for you to find free or low-cost care for you during your pregnancy or delivery. You do not have to be a citizen to qualify, though you will have to meet an income requirement. According to the HRSA, there are no Hill-Burton obligated facilities in Alaska, Delaware, Indiana, Maryland, Minnesota, Nebraska, Nevada, North Dakota, Ohio, Rhode Island, South Dakota, Utah, Vermont, Wyoming, and all the territories apart from Puerto Rico.

Birth centers

If you’re medically low risk, it may be worth looking into the possibility of giving birth in a birth center instead of a hospital. In an AABC study, birth centers were shown to be a safe place to give birth for medically-low risk women. Additionally, birth centers are significantly less expensive than giving birth in a hospital ward and have a high rate of patient satisfaction.

Birth centers are characterized by:

- Having a relaxed and warm atmosphere

- The option to return home shortly after giving birth

- Providers that may include nurse-midwives, direct-entry midwives, or nurses working with an obstetrician

- Being a freestanding facility, on hospital grounds, or inside a hospital

According to Centsai.com, giving birth in a birth center costs around $12,000, whereas giving birth in a hospital costs nearly three times that amount on average. If you cannot get insurance while pregnant and are medically low-risk, it may be worth looking into giving birth in a birth center as opposed to a hospital to save money. According to the American Pregnancy Association, a birth center might not be the right fit for you if you are expecting twins, are diabetic or have preeclampsia.

Additionally, the American Pregnancy Organization recommends asking the following questions (and more) before choosing a birthing center:

- What is the transfer rate of women from the center to the hospital? (7-12% is acceptable)

- In what situations would labor be induced wither with Pitocin or by breaking the amniotic sac?

- Are analgesic drugs used? Are epidurals offered?

- Is there a time limit on the second stage of labor?

- What percent of their women require episiotomies? (less than 10% is normal)

For a longer list of questions, and more information on birthing centers, you can visit the American Pregnancy Organization’s website.

Discount plans for childbirth

One kind of insurance plan that you can get year-round to help cover the cost of your medical care is a discount plan.

These plans offer you discounts on certain health care services, prescriptions, and medical devices – like hearing aids, for example – from in-network providers. These plans can help you save certain percentages on necessary services like prenatal and postpartum care.

These plans are a great low-cost option considering they can cost around $25-$45 per month and offer substantial discounts. For example, with AmeriaPlan’s Deluxe Plus Membership, which is $39.95 per month, you can save up to 80% on wellness screenings, ancillary services, and they can help provide you with a bill negotiator to help you save on medical costs.

Hospital Indemnity Insurance

Another option for those without insurance is a hospital indemnity plan. These plans can help you prepare for the cost of labor and delivery. These plans can also help pay for long term stays in the hospital. This coverage can especially be helpful if you or your baby need to be admitted into the ICU or NICU.

If you think that you may have a complicated delivery, hospital indemnity insurance may be appealing. They are a generally low-cost option considering hospital indemnity plans may pay up to $3,000 per admission (your admission and your child’s admission are separate) while only costing around $45 per month.

Short-term and long-term disability coverage for pregnancy

Another way to help offset the cost of pregnancy and birth is to purchase short-term disability insurance. This type of coverage helps cover the time you’re out of work while pregnant as well as during and post-delivery. If you expect a complicated delivery or twins (or more), short-term or long-term disability coverage may be something you want to consider even though this type of coverage tends to be costly.

Short or long-term disability coverage can supply much-needed income during and after pregnancy. According to the Bureau of Labor Statistics, only around 15% of US workers in 2017 had family leave benefits – even though federal law requires most employers to give workers 12 weeks of unpaid leave.

Most policies pay a six-week benefit for a vaginal birth and an eight-week benefit for a C-section. Most women have to stop working before delivery and some women need to take time off after giving birth because of complications like hypertension related to pregnancy and postpartum depression.

The cost of this type of coverage is a little more expensive as it tends to be a percentage of your annual gross income. You can expect to pay around 1-3% of your annual gross income for disability coverage. However, if you expect to be out of work for a long period, this may be an option to consider.

Self-pay and charity rates

Generally, hospitals offer lower rates to those who are medically needy or who pay for care in cash. They don’t advertise these rates. You’ll need to call and ask to find out about them.

It’s common for hospitals to offer reduced fees for diagnostic procedures – such as x-rays and ultrasounds – as well as lab work. If you expect to pay out-of-pocket for services through a hospital, call and ask if they have a self-pay or charity rate. If you are uninsured or have a high-deductible, you may be able to find significant savings by negotiating with your provider.

Find affordable pregnancy insurance with eHealth

Since pregnancy and giving birth are mandatory health benefits under the ACA, getting affordable maternity health coverage is as simple as finding the right health insurance plan for you and your growing family.

You can start shopping for a health insurance plan that fits your budgetary and coverage needs at any point in the year. However, you can only enroll either during the annual open enrollment period – which runs from November 1st through December 15th in most states – or during a special enrollment period.

eHealth’s intuitive site and licensed health insurance agents help you compare your health insurance plan options to help you find the plan that suits you best. Keep in mind that eHealth’s help is completely free, you will not pay more for a plan purchased through eHealth than you would if you were to purchase it anywhere else. Additionally, eHealth’s agents are always here to help you with questions even after you’ve purchased a plan. You can learn more about pregnancy insurance and health insurance for babies by going online to the eHealth website or getting in contact with one of our licensed agents.

Frequently asked questions about pregnancy insurance

If my doctor is in-network, is my hospital in-network?

Most people assume that since their doctor is covered by insurance that the hospital in which they’re giving birth is also in-network. This is not always the case. Just because an in-network doctor has privileges at a specific hospital doesn’t make the hospital in-network. Additionally, neonatal intensive care units (NICUs) can be contracted by the hospital, which means they may be out-of-network. If your baby ends up going to the NICU and it so happens to be out-of-network, you can end up with surprise out-of-pocket expenses.

Similarly, if you choose to have an epidural, the anesthesiologist may not be in-network. It’s a good idea to call your insurance and make sure they cover the providers you plan to use before you give birth to make sure they’re in-network and you don’t get stuck with any expensive and unexpected medical bills.

Can I get or switch health insurance coverage while pregnant?

You can enroll in health insurance coverage during the annual open enrollment period, which runs from November 1st through December 15th in most states. Some states have extended open enrollment; to learn more about the open enrollment period in your state, check out our OEP by state breakdown.

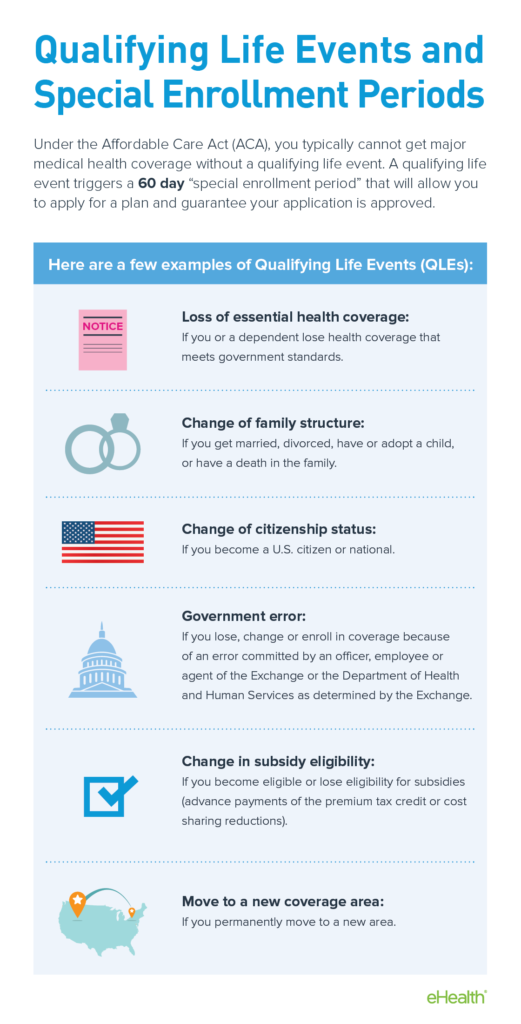

You cannot enroll or change health insurance plans outside of the open enrollment period unless you experience a qualifying life event. A qualifying life event will trigger a special enrollment period, which typically lasts around 60-days. During these 60 days, you may enroll or switch health insurance coverage.

Does short-term health insurance cover pregnancy?

No, short-term health insurance generally does not cover pregnancy or birth. Such plans might be a good option for other non-pregnancy or non-birth needs for those who missed the open enrollment period, are looking for affordable coverage for worst-case scenario situations, and those looking to cover any other gaps in health insurance coverage. Short-term insurance is cheaper than more comprehensive plans that cover pregnancy or birth, but these plans provide much less comprehensive coverage than major medical plans. Unlike ACA-compliant plans, short-term plans can also deny coverage if you have a pre-existing condition or refuse to cover care related to pre-existing conditions. Since pregnancy is still viewed as a pre-existing condition, short-term plans are very unlikely to cover care related to pregnancy or birth.

In a recent Kaiser Family Foundation (KFF) review of 24 short-term health insurance plans offered by two large online providers, none were found to cover maternity care. Additionally, short term plans generally do not cover abortions – which typically cost under $1000 for procedures performed during the first trimester, which doesn’t include the cost of travel and time off work which is an important factor for women who live in states where there is a mandatory waiting period to get an abortion.

While short-term plans can be great options in other situations, they will not help offset the cost of pregnancy and giving birth.

Does pregnancy insurance cover pre-existing conditions?

Pregnancy insurance typically does not cover pre-existing conditions related to pregnancy. These conditions are usually considered as exclusions from coverage due to their pre-existing nature.

Does pregnancy insurance cover complications during pregnancy or childbirth?

Pregnancy insurance often covers complications during pregnancy or childbirth, depending on the specific terms and conditions of the policy. Common complications such as preeclampsia, gestational diabetes, or complications requiring medical intervention during childbirth may be covered under certain pregnancy insurance plans.

How do I enroll in pregnancy insurance?

To enroll in pregnancy insurance, you can typically explore available plans through private insurance companies or healthcare marketplaces. Begin by researching different insurance providers and comparing their pregnancy coverage options. Once you’ve identified a suitable plan, you can enroll online, over the phone, or through a licensed insurance agent. Additionally, if you qualify for government-sponsored healthcare programs like Medicaid, you may be eligible for pregnancy coverage through these programs.